How to Refinance Your Home Loan for Renovations

At Cameron Construction, we totally get it — home renovations aren’t just about new tiles and fixtures. They’re about turning your living space into something spectacular.

Thinking about refinancing your home loan for those upgrades? Yeah, it’s a move that can be as smart as it sounds. It’s like getting your dream projects underway while possibly snagging some juicier loan terms.

This guide? It’s your playbook — we’re gonna break down the refinancing process step-by-step, so you can make savvy, informed decisions about your home improvement plans.

How Home Loan Refinancing Works for Renovations

The Basics of Refinancing

Home loan refinancing-sounds complex, right? But for those looking to jazz up their space, it’s like getting a makeover for your finances. You’re swapping the old mortgage for a new one, and hopefully, it comes with some snazzier terms or a bigger wad of cash to kickoff renovation dreams. Want in?

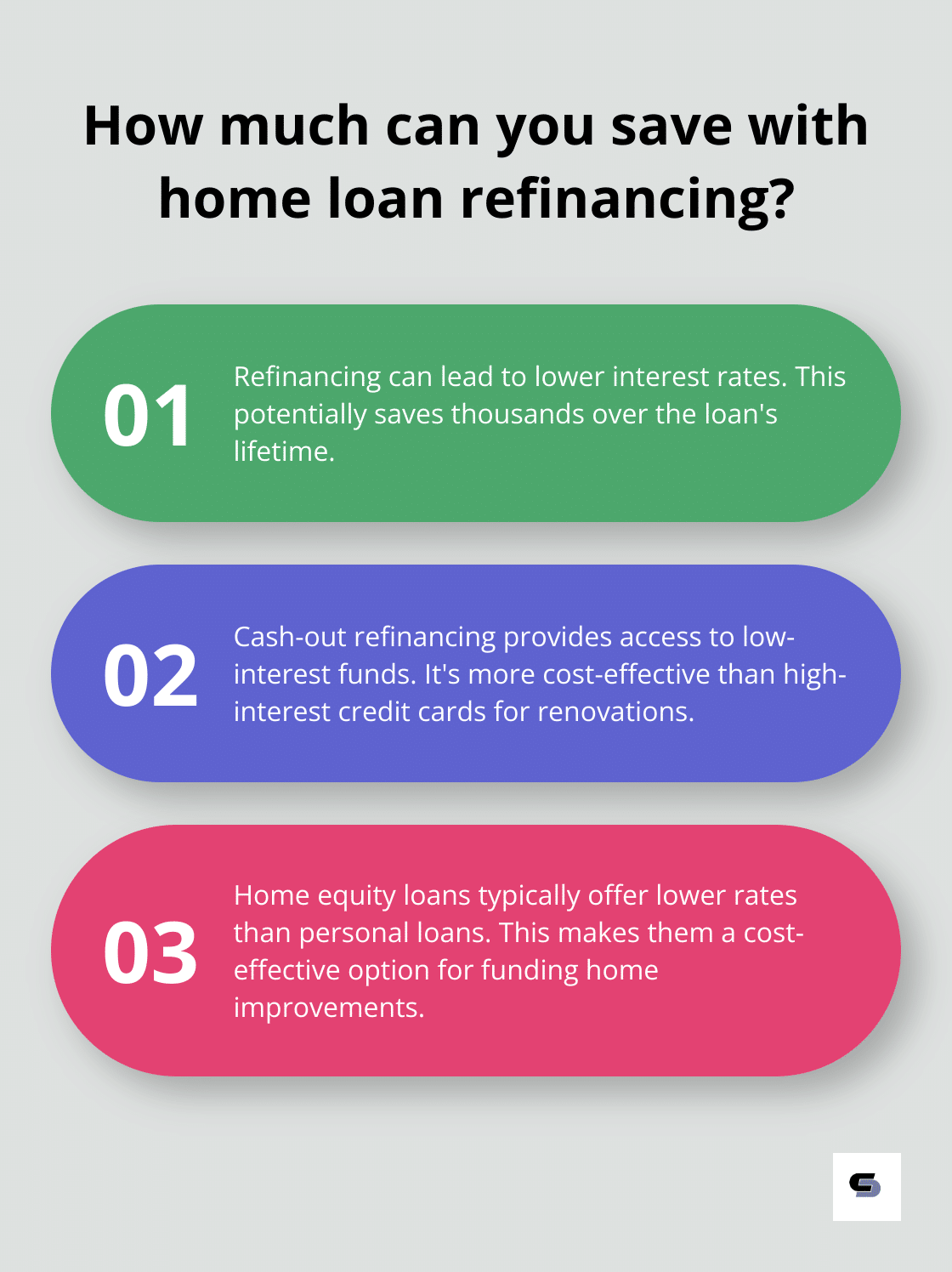

When you refinance, it’s essentially a do-over loan to pay off what you already owe (think of it as hitting refresh). And here’s the kicker-this new deal might offer a lower interest rate or more time to pay back. Renovation time? A cash-out refinance is your ally, giving you access to pretty sweet, low-interest moolah compared to say, those plastic cards with sky-high rates.

Benefits of Refinancing for Home Improvements

So what’s in it for you? Loads of perks:

- Lower Interest Rates: Score a rate better than your old mortgage’s and watch the savings pile up over the loan’s lifetime. Potentially thousands-yes, thousands.

- Cost-Effective Funding: Use that home equity like a boss. Tapping into it could cost you less than other financing-not bad, right? Typically, home equity loans or lines of credit laugh in the face of personal loan rates.

- Increased Property Value: Renovations done right? They’re your golden ticket to boosting that home value sky-high. It’s all about those strategic moves that can balance out the costs over time.

Types of Refinancing Options

Got renovation fever? Here’s a menu of refinancing flavors:

- Rate-and-Term Refinance: Just want to tweak the rate or stretch the loan term? Great for freeing cash for smaller projects when adding funds isn’t on the agenda.

- Cash-Out Refinance: Get a little greedy-borrow more than you owe and use the surplus to build that dream reno.

- Home Equity Loan: It’s like a second chance-a second mortgage giving you a lump sum to tackle big design projects with a fixed budget.

- Home Equity Line of Credit (HELOC): Keep it flexible with a revolving line of adventure-based on your home equity, of course. Handy for those projects that keep changing their minds. Hint: interest might be tax-deductible if it’s for improvement purposes.

Factors to Consider

Done picking a life-changing flavor? First, ponder these:

- Current Equity: How much stake do you hold in your turf? Affects how much you can borrow.

- Credit Score: Aiming for the cream of the crop on loan terms? Up your credit game.

- Long-Term Financial Plans: Before jumping in, think about how refinancing jives with your financial roadmap.

- Closing Costs: And yes-don’t overlook those pesky fees, usually lurking at 2-5% of the loan.

- Loan Term: Longer terms equal smaller payments but watch out for ballooning total interest.

The Refinancing Process

Here’s a cheat sheet on navigating the refinancing waters:

- Application: Start the dance with your lender of choice-loan applications kick it off.

- Appraisal: A little home value check-let your lender size up your investment.

- Underwriting: Hold your breath as lenders dissect your financial vitals and either greenlight you or send you back to the drawing board.

- Closing: Dot those I’s, cross those T’s on new loan documents, and cough up any related fees.

Now that you’ve peered behind the curtain of refinancing for renovations, it’s time to roll up the sleeves. You’re ready to dial in on the nitty-gritty, marching towards that dreamy home makeover. Is that the sound of a toolbox opening? Let’s hustle and make these plans a reality.

How to Refinance Your Home Loan

Refinancing your home loan for renovations – sounds like a mouthful, right? But it’s all about careful planning and execution. Here’s your guide to navigating this maze effectively.

Assess Your Financial Health

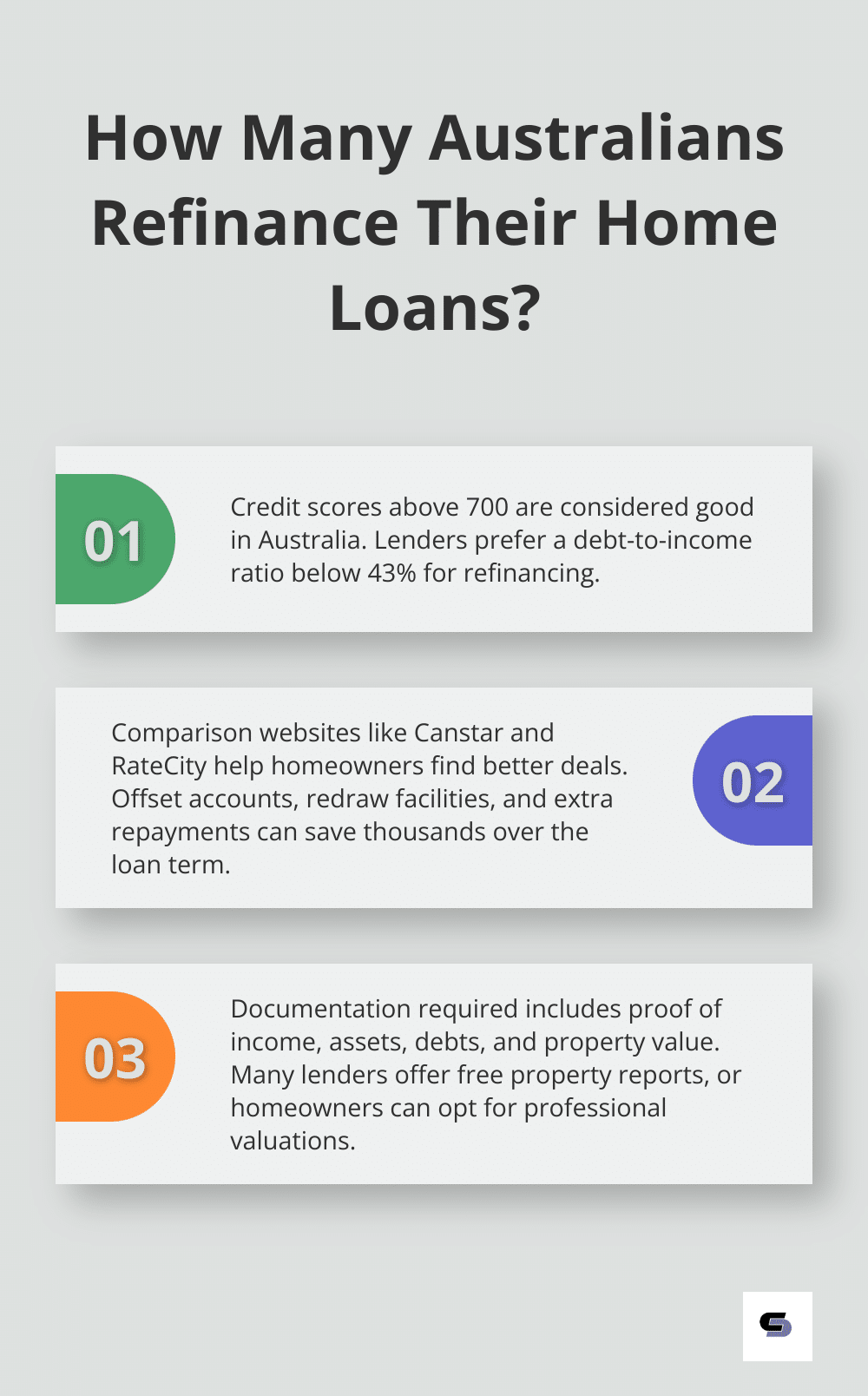

First things first, dive into your finances. Peek at your credit report and score. For the Aussies out there, a score over 700 (according to Equifax) is gold. If you’re sitting below that line, time to polish it up a bit before you jump into refinancing. Tackle those pesky debts or fix any hiccups on your credit report.

And let’s not forget the debt-to-income ratio – lenders love it below 43%. If you’re over the line, consider trimming some of that debt before you make any moves with refinancing.

Shop Around for the Best Deal

Here’s a tip: don’t just stick with your current lender. Using comparison websites like Canstar or RateCity is like having a financial shopping spree at your fingertips.

And don’t get blinded by interest rates. Look at the full package – offset accounts, redraw facilities, and the magic of extra repayments. These little gems can shave thousands off your loan over time.

Prepare Your Documentation

Lenders want the usual: proof of income, assets, debts. Gather those pay slips, tax returns, bank statements, and the nitty-gritty details of loans or credit cards. If you’re self-employed, get those business financial statements in order.

And you’ll need the skinny on your home’s value. Many lenders toss out free property reports, or you could shell out for a pro valuation. It’ll give you the lowdown on your equity and borrowing power.

Navigate the Application Process

Picked a lender? Nice. Time to submit that application. Many lenders are in the 21st century now with online applications, smoothing the wrinkles in the process. Be ready for them to ask for extra docs or to clarify things as you go through underwriting.

Get approved, and bam – loan offer on the table. Read it like it’s a best-seller. Check the interest rate, fees, and terms. Don’t be shy – haggle a bit.

The grand finale is settlement, where your new loan kicks the old one to the curb. This is also when you’ll get any extra cash for your reno (if a cash-out refinance is your thing).

Consider Professional Advice

You’re not just hunting for the lowest rate. You want a loan that vibes with your financial goals and renovation plans. Chat with a financial advisor or mortgage broker. They can dish out insights that’ll help you make those smart choices based on your unique situation.

With a killer refinancing strategy, you can live out your renovation dreams, boosting both the comfort and value of your home. Ready for the next step? Let’s dive into maximizing your refinancing for renovations, coming up in the next section.

Maximizing Your Renovation Budget

Setting a Realistic Budget

So you’re thinking about refinancing your home loan for renovations? Buckle up… you’re about to start quite the journey. And crucial step #1? Stretch every dollar like it’s yoga. A killer budget is your best friend in the chaos of renovation.

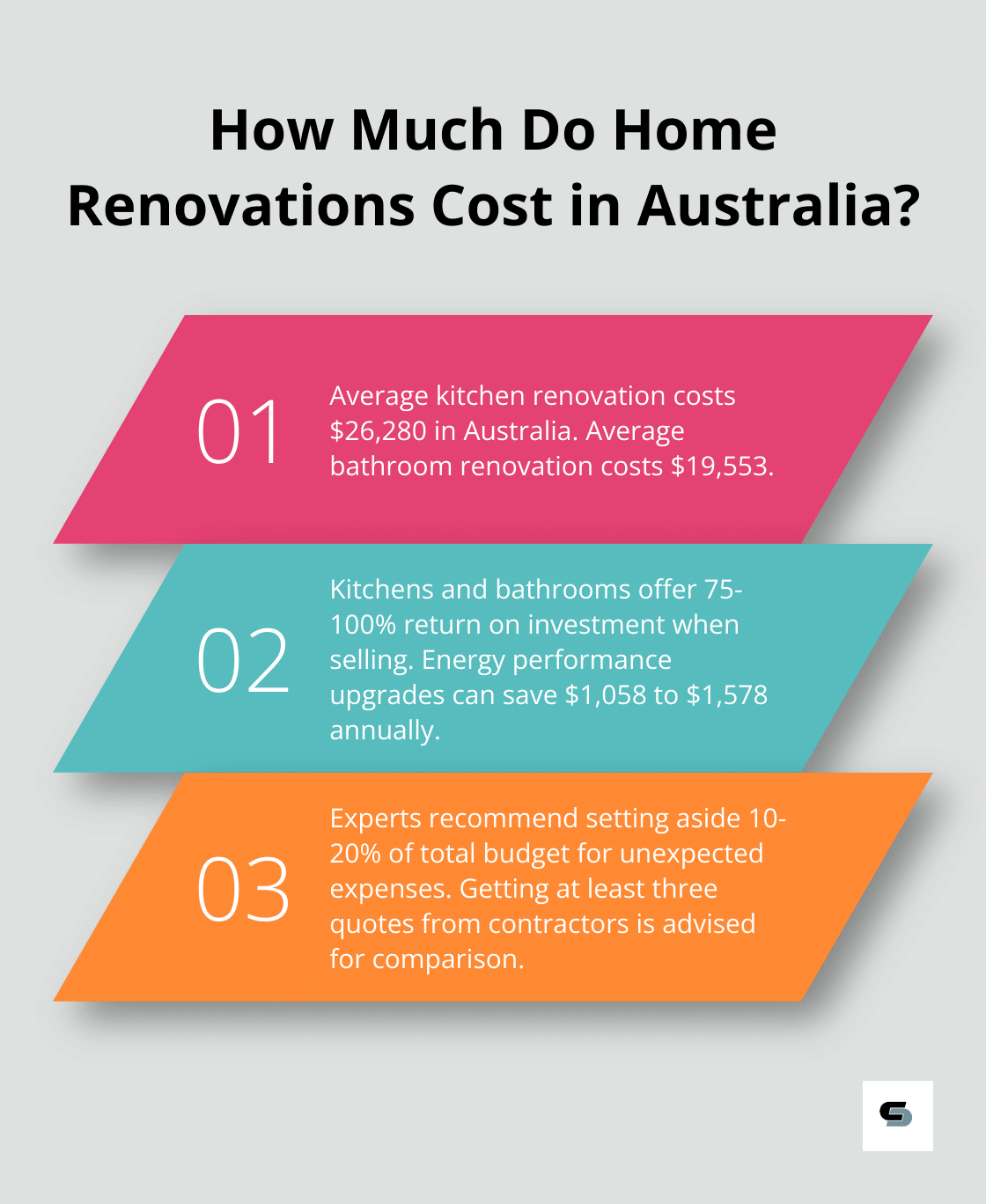

Now, according to the Housing Industry Association, the average kitchen update down under will set you back around $26,280, and sprucing up a bathroom averages about $19,553. Use these numbers as your cheat sheet, but remember – your costs might do their own thing based on what you want and how you want it.

First things first, snag some detailed quotes from a crowd of contractors. Three or more should do the trick for solid comparison. The cheapest option? Tempting, right? But hold up. Your game plan is to find the sweet spot between quality and pocket-friendliness.

Oh, and throw in a “yikes, didn’t see that coming” fund of about 10-20% of your total budget. Old homes love to throw curveballs – think ghostly wiring or ninja water damage. This cushion keeps you from panicking when surprises pop up (and they will).

Prioritizing Home Improvements

Here’s the scoop: not all renovations love you back equally when it comes to selling your home. Realestate.com.au spills the beans that kitchens and bathrooms tend to offer the best bang-for-your-buck, recouping like 75-100% of the costs when you sell.

But… don’t let ROI hog the spotlight. Think about what puts the cherry on top of your everyday life. A home office? Might not skyrocket your property value, but could massively skyrocket your work-life mojo.

Then you have the stealthy heroes – energy-efficient upgrades. These often fly under the radar but can deliver killer long-term savings. Check out energy performance upgrades – potential yearly savings between $1,058 and $1,578 from year one. Think double-glazed windows, solar panels, or insulation that’s built like a tank to juice up your energy savings.

Exploring Additional Financing Options

Refinancing is cool, but bigger renovations might need a little side hustle. Enter construction loans – the trusty steeds for major makeovers. Access funds gradually, pay interest only on what you’ve used. Not bad, huh?

Or consider a line of credit – like a credit card on steroids secured against your home equity. Flexibility’s great, but play it smart. Manage it like a pro.

Got smaller dreams for your place? Look at personal loans or credit cards with a sweet interest-free intro. But Beware… high-interest options can be sneaky. Craft a clear repayment roadmap to dodge any financial mess.

Choosing Quality Materials and Fixtures

Here’s where the rubber meets the road – selecting killer materials and fixtures. Cutting corners here? Big mistake. Quality stuff might make your wallet groan initially, but consider it an investment in future coolness and less hassle.

Aim for the perfect combo of durability and wow-factor. High-traffic zones like kitchens and bathrooms – go for porcelain tiles, quartz countertops, and solid wood cabinetry. Costs more? Yep. Outlasts the cheap stuff? Absolutely.

Working with Professionals

DIY projects sound like a good idea until reality hits. Some renovation gigs need the pros on deck. Experienced contractors, architects, designers – these folks will save you from mistakes that’ll make your wallet cry, plus make sure everything’s on the right side of the law.

Pro advice isn’t just about rules and regulations – it’s your roadmap to making killer decisions on layout tweaks, material choices, and budget stretching. They can often pull off creative, cost-effective tricks you never even had on your radar.

Final Thoughts

Refinancing your home loan to bankroll renovations-yeah, it’s a game changer. Upgrade your digs and maybe, just maybe, snag better loan terms while you’re at it. Digging into your home’s equity means tapping into cash at rates that don’t make you hyperventilate (compared to other options that might). But, but, but … you gotta get a close-up of your finances first. Check your credit score, debt-to-income ratio, and long-term financial goals before you jump in.

Look, when it comes to refinancing and dialing up the reno game, professional advice is the non-negotiable MVP. Financial advisors, mortgage maestros, and contractors worth their salt deliver the insights you need to not get blindsided. Map out a budget that’s anchored in reality, figure out what renos top the list, and throw in a buffer just in case things go south (because you do not want to cut corners on quality, especially in spaces that take a beating or major structural tweaks).

If you’re in Melbourne and feeling the itch to get started on this home reno adventure, Cameron Construction has got your back. With experience deep in transforming homes, their crew can help steer your project ship, making sure it lines up with what you’ve been dreaming of. Refinancing your home loan for renos is a two-for-one deal-your future comfort and your beloved home’s potential.